Introduction

The dynamics of house prices over the past 8 years have been largely determined by the evolution of interest rates, and through them, the cost of mortgages. The general tendency is that low borrowing costs lead to an increase in house prices, while high borrowing costs are associated with stagnating or falling house prices.

To illustrate the relationship, we chose to compare the cost of loans indicator of the National Bank of Hungary (MNB) and the aggregate housing price index of the Hungarian Central Statistical Office (KSH) over time. The MNB’s cost of loans indicator includes all other costs in addition to interest rates, making it suitable for a time-series comparison of the cost of housing loans. The analysis of the cost of credit is also relevant, because a significant share of housing market transactions (41 percent on average between January 2018 and February 2024) is made with loans.[1] This implies that the cost of housing loans is a major determinant of housing market prices, as it is a shaper of the demand side.

The KSH’s aggregate housing price index is based on the main data for 94 percent of housing transactions between private individuals in both 2022 and 2023.[2] Thus, it is representative of housing market trends. In line with Eurostat, the KSH housing price index shows the evolution of housing market prices relative to the base year of 2015. To compensate for inflation, the KSH’s real house price index was used.

Interest rates and prices

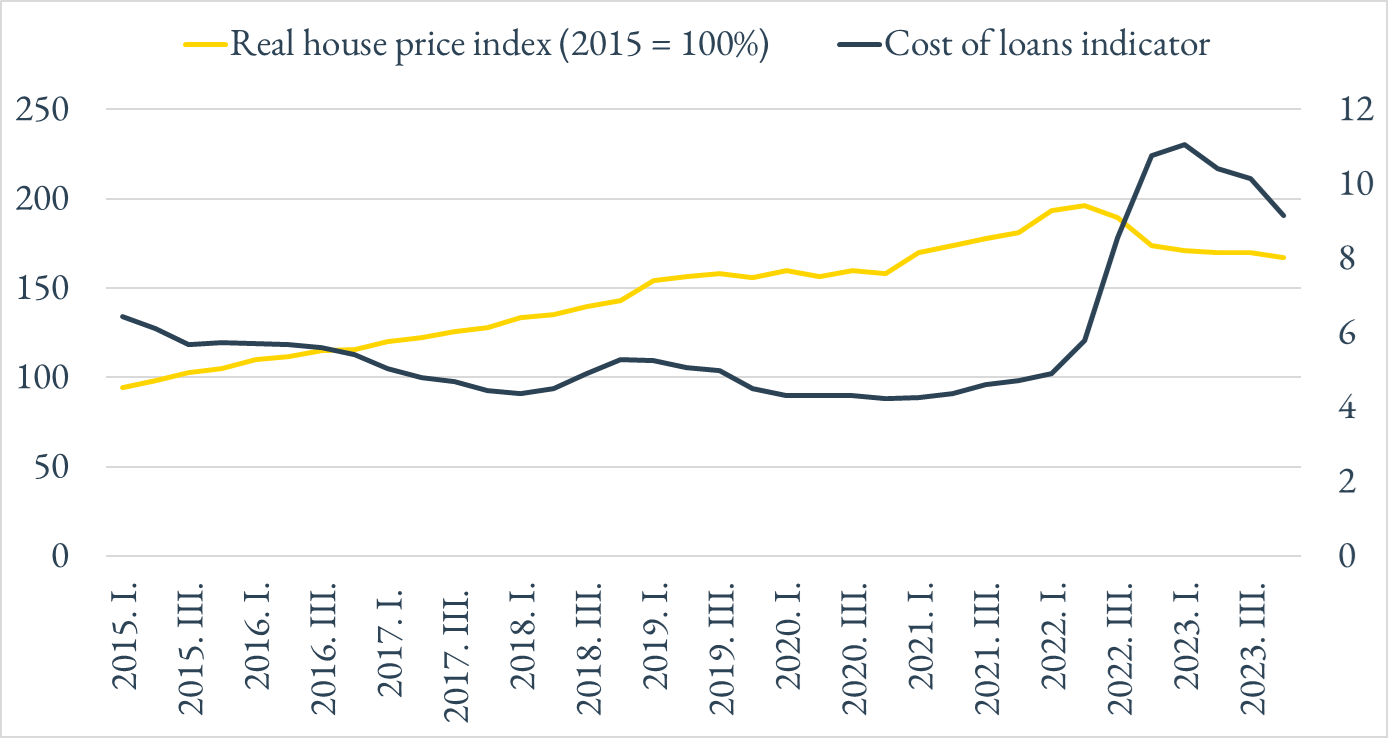

Comparing the data, we can see that the value of the MNB cost of loans indicator gradually declined from 2015 until the end of 2017, with a period of stagnation, which is a good reflection of the low interest rate environment at the time. During the same period, the real value of house prices also increased steadily. A short period of stagnation was observed only after the first three quarters of 2018, when the cost of loans started to rise. The most striking impact was the gradual increase in borrowing costs since the end of 2020, particularly the cost increases experienced in the first three quarters of 2022, with a rise of 48 percent in the second quarter of 2022, followed by a 26 percent increase in costs. Figure 1 shows that despite the gradual loan cost declines, the real house price index fell in 2023. This was because interest rates were still too high, compared to historical levels.

Trends in the real house price index and the MNB cost of loans indicator (right hand scale) (2015-2023)

Real house prices have stagnated or fallen in recent quarters, due to a significant rise in borrowing costs

The effects of the evolution of the cost of loans

As long as borrowing costs were favorable, the number and value of loans disbursed increased steadily, as low interest rates meant that more and more people could afford to take out mortgages.[5] At a time when the cost of credit was rising sharply, the volume and value of loans for home purchases also fell.

Figure 2 shows that between 2015 and 2021, the cost of loans has gradually decreased, while the value of housing loans disbursed has increased year on year. This ended in 2022 with a 67 percent jump in loan costs, resulting in a 7 percent fall in value, and then in 2023 loan costs also rose, by 36 percent compared to the previous year, resulting in a 49 percent fall in the value of loans disbursed.

Trends in the value of housing loans disbursed and the MNB cost of loans indicator (right hand scale) (2015-2023)

As the cost of loans rises, the value of loans disbursed falls

Loans and house prices

The increase in the value of loans has a positive impact on house price developments. Compared to the previous year, we have observed a decline in the value of loans disbursed for housing in 2023, which may be one of the reasons for the fall in the real house price index in 2023.

Figure 3 below shows that while the value of housing loans disbursed has increased, so has the value of the real house price index. The trend in house prices persisted into 2022, when the value of loans disbursed had already fallen, compared to the previous year. In 2023 the almost 50 percent fall in loan values was followed by a fall in the real value of housing.

Trends in the value of disbursed loans and the evolution of the KSH real house price index (right hand scale) (2015-2023)

The evolution of the real housing market index follows the evolution of the value of disbursed loans

Mortgage maturities and house prices

It is not only lower borrowing costs that are expanding the demand side of the housing market. The increase in mortgage maturity rates also helps to make increasingly expensive housing more affordable, as the loan repayments are spread over more months. This in turn can lead to lower average monthly repayments.

According to data from the Hungarian National Bank, the average maturity of mortgages taken out to finance new homes was 18.5 years in January 2018. This increased by 18 percent to 21.6 years by January 2024. A similar trend can be observed for second-hand housing, where the maturity increased by 17 percent from 16.7 years to 19.6 years. [9]

Trends in the average maturity of mortgages for financing new and second-hand housing and the KSH real house price index (right hand scale) (2018-2023)

As the average maturity of housing loans increases, real house prices are also rising

Figure 4 above shows that high mortgage maturities are generally accompanied by a higher real house price index. This can be explained by the fact that longer maturities allow home buyers to borrow larger amounts at lower monthly repayments. This in turn contributes to rising house prices through increasing housing demand.

Conclusion

In our analysis we have examined the main factors shaping the demand side of the housing market and influencing the evolution of housing prices. We found that one of the determinants of real house prices is the level of borrowing costs. When borrowing costs are low, housing prices rise, while when borrowing costs are high, prices stagnate or fall. This phenomenon is explained by changes in the value of loans disbursed.

We also pointed out that the increase in the average maturity of mortgages also leads to an increase in housing market prices. Longer maturities allow borrowers to borrow larger amounts at lower monthly repayments. This increases the demand in the housing market, which further drives up prices.

[1] Magyar Nemzeti Bank (2024): Lakáspiaci jelentés, 2024. május. https://www.mnb.hu/kiadvanyok/jelentesek/lakaspiaci-jelentes/lakaspiaci-jelentes-2024-majus (Downloaded on: 2024. 07. 30.)

[2] Központi Statisztikai Hivatal (2024): Lakáspiaci árak, lakásárindex, 2023. IV. negyedév, Módszertani megjegyzések.

https://www.ksh.hu/s/kiadvanyok/lakaspiaci-arak-lakasarindex-2023-iv-negyedev/modszertan.html (Downloaded on: 2024. 07. 30.)[3] Központi Statisztikai Hivatal (2024): Lakáspiaci árak, lakásárindex, 2023. IV. negyedév. https://www.ksh.hu/s/kiadvanyok/lakaspiaci-arak-lakasarindex-2023-iv-negyedev/index.html (Downloaded on: 2024.07.30.)

[4] Magyar Nemzeti Bank (2024): Sajtóközlemény a háztartási és a nem pénzügyi vállalati kamatlábakról 2024. április.

https://statisztika.mnb.hu/sk-haztartasi (Downloaded on: 2024.07.30.)[5] Központi Statisztikai Hivatal (2024): 18.1.1.16. Lakáscélú hitelek. https://www.ksh.hu/stadat_files/lak/hu/lak0016.html (Downloaded on: 2024.07.30.)

[6] Magyar Nemzeti Bank (2024): Sajtóközlemény a háztartási és a nem pénzügyi vállalati kamatlábakról 2024. április.

https://statisztika.mnb.hu/sk-haztartasi (Downloaded on: 2024.07.30.)[7] Központi Statisztikai Hivatal (2024): Lakáspiaci árak, lakásárindex, 2023. IV. negyedév. https://www.ksh.hu/s/kiadvanyok/lakaspiaci-arak-lakasarindex-2023-iv-negyedev/index.html (Downloaded on: 2024.07.30.)

[8] Magyar Nemzeti Bank (2024): Sajtóközlemény a háztartási és a nem pénzügyi vállalati kamatlábakról 2024. április. https://statisztika.mnb.hu/sk-haztartasi (Downloaded on: 2024.07.30.)

[9] Magyar Nemzeti Bank (2024): Lakáspiaci jelentés, 2024. május. https://www.mnb.hu/kiadvanyok/jelentesek/lakaspiaci-jelentes/lakaspiaci-jelentes-2024-majus (Downloaded on: 2024.07.30.)

[10] Központi Statisztikai Hivatal (2024): Lakáspiaci árak, lakásárindex, 2023. IV. negyedév. https://www.ksh.hu/s/kiadvanyok/lakaspiaci-arak-lakasarindex-2023-iv-negyedev/index.html (Downloaded on: 2024.07.30.)

[11] Magyar Nemzeti Bank (2024): Lakáspiaci jelentés, 2024. május. https://www.mnb.hu/kiadvanyok/jelentesek/lakaspiaci-jelentes/lakaspiaci-jelentes-2024-majus (Downloaded on: 2024.07.30.)